Date

17 Jul 2020Category

TaxSubject to Royal Assent, Finance Bill 2019-20 is expected to introduce significant changes for some trusts holding non-UK situs property which was settled by a non-UK domiciled settlor. The background and context of these changes was covered in our previous insight issued following the publication of the draft legislation in July 2019 (click here to read).

Throughout the current insight, references to deemed domicile do not include deemed domicile status as a result of being a formerly domiciled resident (born in the UK with a domicile of origin in the UK), where different rules apply.

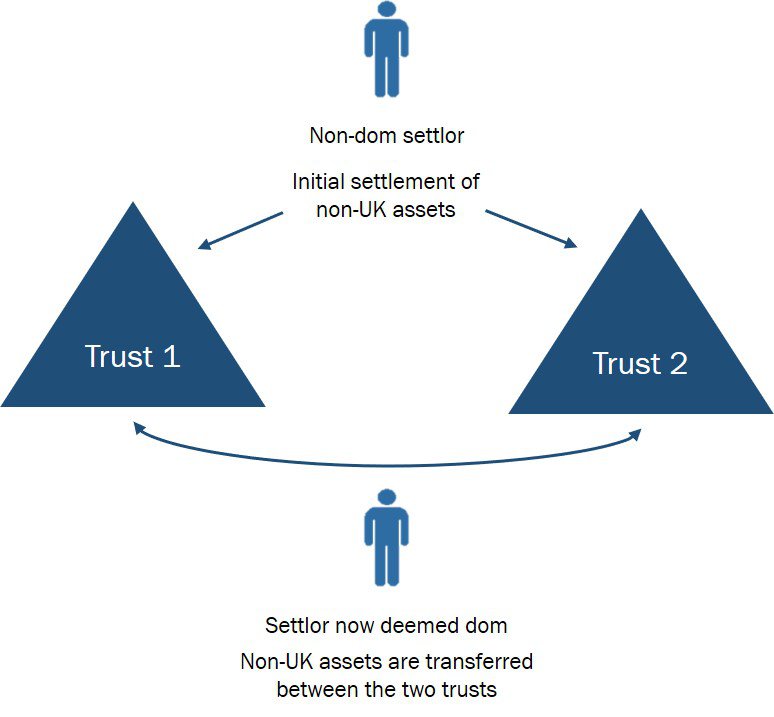

The trust changes are primarily targeted at the two following scenarios.

In this scenario, the legislation confirms that, while the initial settlement remains excluded property for inheritance tax (IHT) purposes, the additional settlement will be within the scope of UK IHT as it is made while the settlor is deemed UK domiciled. The additional funds settled will be subject to 10-yearly IHT charges and to IHT exit charges on property leaving the trust. The same would apply if the settlor had acquired an actual UK domicile by the time the second settlement was made.

This had always been HMRC’s view and is now being put on a statutory footing. There is a specific exclusion for accumulations of income made after the settlor has become UK domiciled or deemed UK domiciled.

The assets transferred will no longer qualify as excluded property for IHT purposes if they are transferred between trusts when the settlor is UK deemed domiciled or actually domiciled.

There are concerns that, to some extent, the new legislation has a retrospective affect and could alter the tax treatment of actions which have been taken in the past.

Scenario 1 – in this scenario, the additional settlement made when the settlor was UK domiciled or deemed UK domiciled will not be excluded property for IHT purposes, regardless of whether it was made before or after the date of Royal Assent for Finance Act 2020. This is perhaps not surprising given that the legislation merely giving a statutory footing to HMRC’s historic published view.

Scenario 2 – there is protection in the legislation for trust to trust transfers which are made before the date of Royal Assent and these will not be brought within the relevant property regime (meaning that the assets will not be made subject to 10-yearly IHT charges and IHT exit charges). However, the transferred assets will lose their protection for ‘gift with reservation of benefit’ purposes. This means that if the recipient trust is settlor interested, the transferred assets will fall within the settlor’s estate for IHT purposes from the date of Royal Assent onwards.

The new legislation could also catch loans made to trusts by a settlor (or potentially other parties). Loans are deemed to result in property becoming comprised in a settlement and a strict application of the legislation means that trust property deriving from loans received while the settlor is UK domiciled or deemed UK domiciled will not qualify as excluded property for the purposes of both the relevant property regime and the gift with reservation of benefit rules.

A deduction may be available for the liability of the loan, but this will be subject to stringent rules on the deductibility of debts and allocation of liabilities.

The second reading of Finance Bill 2019-21 in the House of Lords is scheduled for 17 July 2020 and it is likely that Royal Assent is imminent.

As a matter of urgency, the trustees of trusts settled by non-UK domiciled settlors who have become domiciled or deemed-domiciled in the UK should consider if they have any trusts which fall into the following categories:

More generally, trustees should undertake a wider review of excluded property trusts where the settlor has now become either UK domiciled or deemed UK domiciled to ensure that they are fully aware of the effect of the changes on each trust. If property has been added to a trust (or transferred between trusts) while the settlor is UK domiciled or deemed domiciled, this could taint the trust for income tax and capital gains tax purposes as well as having IHT implications. In some situations, such tainting could result in trust income and capital gains becoming taxable on a UK resident settlor on an arising basis. Trustees need to be aware of the tax issues associated with each trust and ensure that relevant deadlines (such as 10 year charge dates) are monitored.

Should you wish to enquire further into these areas please get in touch with your normal Wilkins Kennedy contact or a member of our tax team.